Post-COVID Healthcare: Landscape Outlook & Implications for Private Equity Firms

Private equity investment has grown dramatically over the last decade, becoming a larger source of industry capital across buyout, growth, and venture strategies. Estimated annual deal values have gone from $41.5 billion in 2010 to $119.9 billion in 2019, for a total of approximately $750 billion over the last 10 years. Healthcare represented 14 percent of deal activity in private equity last year, up from 9 percent in 2007. Such an explosive growth is driven by increasing healthcare expenditure, huge pool of uninvested capital already dedicated to private equity funds as well as market disruption triggered by the pandemic.

Despite its globally emerging market and extending impacts, healthcare remains one of the least digitized industries. According to UBS Investment Bank, private equity investors are at immense investing opportunities, with a whopping of 146,000 private firms worldwide dwarfing the 2,700 publicly traded health-care companies. With hundreds of deals being closed annually, US’s market is the most blooming with half of the buyouts globally.

“The universe of potential investable companies for private equity is larger,” UBS said. “Private equity is a primary source of capital for innovation, especially for early-stage drug discovery where corporate funding is often scarce.”

These firms are potential to reinforce “highly fragmented and high-margin businesses” within health-care services. “Private equity sponsors can provide exposure to innovative companies developing next generation therapies,” UBS said, complementing that private equity investments “have accelerated rapidly in the life science sector.”

Like most of other industries in the US, healthcare sector was heavily wrecked by the pandemic which consequently suppressed the private equity investing. However, with an increasing demand for healthcare of an aging population and rising chronic disease, PE investors in healthcare quickly returned to the market with optimistic opportunities.

A Look Back on Healthcare Private Equity Deals

With a promising future bearing transformational activities, many seasoned PE investors doubled down on healthcare in 2020 in the search for intriguing targets. Blackstone, for example, acquired HealthEdge, Cryoport, and Precision Medicine Group to enhance its portfolio, as well as ZO Skin Health, a cosmetics company with potential healthcare applications. Many funds also used add-on assets to bolster the capabilities of their current portfolio companies. International firm like Advent was able to expand the home health services of its AccentCare asset through the acquisition and merging with Seasons Hospice.

Private equity firms have targeted health care investments for an array of reasons, most having to do with their potential profits. Health care drives a huge part of the nation’s economic output — almost 20 percent of gross domestic product. In addition, health care is a fragmented business with many small operators like physicians; private investors often find outsize gains in industries in which they can create economies of scale through consolidation.

Healthcare providers and biopharma remain the largest focus for the investing landscape, accounting for more than 70% of the deals. Certain provider segments, including behavioral health, women’s health, veterinary medicine, and home care gained additional momentum in 2020. Meanwhile, biopharma services continued to generate the strongest interest from experienced private equity sponsors looking at this sector with traditional hunting grounds like contract research organizations (CRO) or outsourced commercialization services. New York-based PE firm Kohlberg and Abu-Dhabi-based Mubadala have acquired a majority stake in PCI Pharma Services, an integrated pharmaceutical supply chain solutions company or Blackstone investing in Cryoport to take advantage of its cell & gene therapy logistics, just to name a few.

Opportunities for Healthcare Investing in 2021 and Beyond

So, what are the opportunities waiting for the healthcare sector and its investors in 2021 and beyond? Let’s read on to find out.

Telehealth

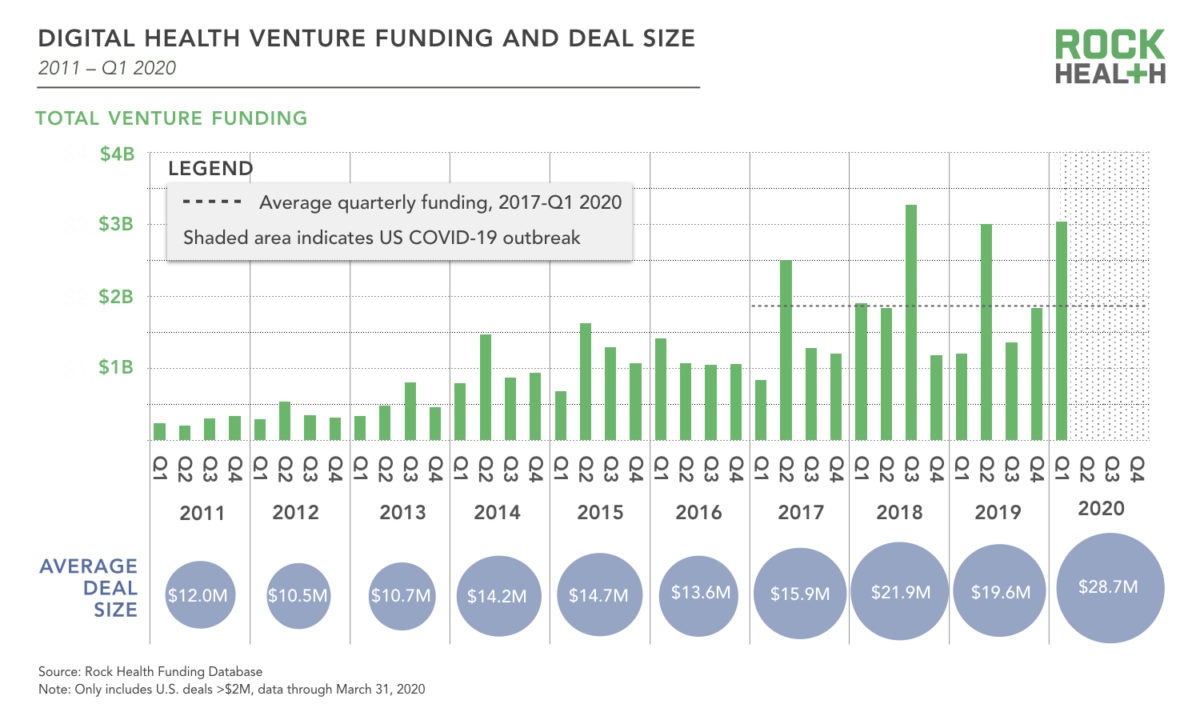

In a time when patients were not able to see physicians face-to-face due to the infectious nature of COVID-19, many people experienced their first-ever virtual visit. Telemedicine visits skyrocketed from only 1-2% of ambulatory care visits pre-pandemic to 30% of all visits. Investment in telemedicine solutions nearly tripled between 2019 and 2020, growing from $1.1 billion to $3.1 billion.

“COVID-19 effectively funded the trial and adoption of digital health/telemedicine technology,” reflected Aaron Martin, executive vice president and chief digital officer at Providence. “Tens of millions of patients were forced by circumstance and safety to sample this new digital approach to healthcare and they liked it. This advantages disruptors because they don’t need to spend the marketing dollars to get patients into the market. Health systems and plans need to quickly make investments in digital or be left behind.”

Beyond higher utilization, investments in telemedicine are being driven by changes in reimbursement policy from both government and private payers. It quickly became clear that telehealth can drive efficiency and improve cost, while allowing expanded access to care and reduced patient demand on facilities. Preventative care can also reduce avoidable readmissions to the emergency department—by engaging patients more frequently at a lower cost.

Remote Patient Monitoring

Wearables and digital health tools will play an increasingly essential role in monitoring patients, providing support, and tracking behaviors—all from the comfort of patients’ home. The rise of digital biomarkers has the potential to enable remote diagnostics and broaden the scope of remote patient monitoring (RPM) applications.

Total funding for RPM solutions more than doubled in 2020—from $417 million to $941 million. Like telemedicine, this growth was supported by changes in reimbursement models. Healthcare investors believe RPM tools for chronic care management will ramp up in 2021. As value-based care continues to gather steam, these tools help expand physician access to patient data and enable preventative care models. Proven during COVID-19, access to longitudinal patient data can help with patient triage to downstream services and enable more proactive care.

Behavioral Health Technologies

The investment in recording, reporting, and receiving mental health care has increased in these unprecedented times. In the United States, 50 million people suffer from mental illness, a statistic that has risen due to the ongoing pandemic, with its anxiety, financial hardship, and isolation. The need for help has spiked among consumers and in the healthcare workforce, with burnout and post-traumatic stress disorder. Hope is seen in technology, with funding for mental health solutions increasing from $599 million to $1.4 billion in 2020, driven by investments from the financial community as well as governments, health systems and education.

Bob Kocher and Bryan Roberts of Venrock see the impact and the opportunity in greater access to behavioral healthcare and tech-enabled care for more complex mental health needs. They noted that an increase in access and the use of mental health resources can potentially result in lower employee turnover as well as overall lower medical care costs.

Testing, Tracking and Diagnostics

Healthcare investors and innovators are excited about adding additional value to diagnostic technology. “That early knowledge of a disease or change in health status needs to automatically trigger the next appropriate action,” said Matty Francis, principal in strategic investing with Healthbox, a HIMSS Innovation Company. “If I need a recent negative COVID-19 result or proof of vaccination to board a flight or send my child to school, how can I effectively get that information to the appropriate third parties?”

With the necessity to manage large-scale distribution and testing for COVID-19, testing and tracking technology became ever more essential in 2021 and beyond. This sparked a wave of novel approaches to triaging and tracking large groups of patients and community members. These platforms can adapt to changing conditions and serve as a foundation for population-level tracking in the future.

Consumer-Driven Digital Health

Patients expect the same level of accessibility to healthcare products and services as they do to digital, retail, and financial services. They want a unified digital experience for booking appointments, requesting prescriptions, and receiving follow-up messages.

To create that patient journey, the digital health industry is challenged to seamlessly integrate data between electronic medical records and technology platforms. Healthcare investors are watching for solutions that combine customer experience lessons from tech leaders with effective healthcare delivery.

Health Equity and Community-Centric Innovations

When it comes to marginalized groups in the US, the government’s responses to the pandemic showed exposed cracks in the healthcare business. As societal consciousness shifts, digital health enterprises are beginning to address previously unmet requirements for underprivileged populations. As a result, future solutions that include risk-sharing models to match results, particularly for Medicare and Medicaid populations, are attracting the attention of healthcare investors.

“Health systems will have to start to think differently about their areas of responsibility and jurisdiction… with more of this public health lens,” said Dr. Subaiya. “Now we have to think about the community at large, or the city at large, or the state at large. These shifting boundaries for how you define a market will make things interesting for health plans and health systems. In an era of communicable disease, it’s not just about the member or patient, it’s their whole household, where they live, where they work. So that’s a big implication for markets.”

What’s the Downsize?

While private equity firms can provide capital for innovation or operational acumen for undermanaged hospitals and medical offices, the overwhelming involvement of PE investors pose certain threats to healthcare providers and patients. As the core of private equity investments is to maximize short-term profits for significant returns within 3 to 5 years, firms usually leverage debt financing to raise large sums of capital, leaving the healthcare companies with economic pressure that may be addressed ahead of patients’ welfare.

Private equity acquisition can also counter the goals of helping patients and workers. Research shows that PE ownership was associated with lower frontline nurse staffing which was a major component of nursing home operating costs. Besides, when private equity firms acquire nursing homes, the quality-of-care declines markedly. When COVID-19 struck, hospitals affiliated with private equity firms were among the first to reduce practitioners’ salary and benefits because the operations could no longer make money on elective surgical procedures postponed due to the epidemic. The heavy debt loads typically associated with private equity-owned businesses hinder their ability to withstand profit downturns.

Private equity-owned firms also use practitioners with less experience or training to save money, say doctors associated with the American College of Emergency Physicians and the American Academy of Emergency Medicine.

Because such extenders have less training under their belts, their costs are well below those associated with physicians. In general, employing three extenders equals the cost of one physician, said Robert McNamara, professor and chairman of emergency medicine at Temple University and chief medical officer of Temple Faculty Physicians.

In addition, some medical professionals believe that private equity’s increased engagement in health care in recent years has contributed to shortages of ventilators, masks, and other COVID-19-fighting equipment, because stocking such items costs money. To private equity, this is equivalent to stacking dollar bills on a shelf.

Increasing private equity acquisitions can also lead to antitrust and competition issues. FTC Commissioner Rohit Chopra has recently raised the alarm about the impact of private equity on competition across all sectors of the economy, stating that he is “concerned about the unreported roll-ups in the healthcare sector” and noted that “through these strategies, private equity sponsors can quietly increase market power and reduce competition.”

In the healthcare industry, increased concentration and anticompetitive behavior by providers and suppliers lead to lower quality, potentially crippling bills for patients, and higher rates negotiated with insurers, which are then passed on to patients and employers in the form of higher premiums, co-pays, and co-insurances.

TeamHealth, for example, was featured last year in a report by MLK50 and ProPublica for aggressively suing poor patients who had been unable to pay their emergency room bills. “We should not be running our healthcare system as a profit-making operation on steroids,” said Eileen Appelbaum, an authority on private equity and co-director of the Center for Economic and Policy Research. “Health care is not so much anymore about taking care of patients. It’s way more about making money.”

Would It Be Different under the Biden Administration?

The newly-elected president Joe Biden, who played a key role in the passage of the Affordable Care Act in 2010, is bound to change healthcare policy in 2021 and beyond. Even here, however, the continuities are likely to be as or more significant than the changes.

The likelihood of a divided government should the Senate stay within Republication hands has calmed many of private equity players’ biggest fears, such as a huge hike in the capital gains tax rate.

Many other objectives are likely to be curtailed as well. For example, Health and Human Services Secretary-designate Xavier Becerra pushed for a law in California that gives the state’s attorney general — currently Becerra himself — an effective veto over private-equity healthcare purchases. The idea, however, failed to pass even with Democratic supermajorities in the California legislature and appears unlikely to gain national traction.

Biden’s team is anticipated to place a greater emphasis on social determinants such as providing nutritious meals and transportation services, opening up new investment opportunities. In addition to those areas, investors have their eye on payer services and population health data technologies.

Biden is also expected to take over the Center for Medicaid and Medicare Innovation, which the Trump administration warmly embraced as part of the Affordable Care Act. The topic of healthcare antitrust is one area where the Biden administration is likely to be considerably more aggressive than Team Trump. Even yet, panelists believe it is unlikely to be as damaging to private equity as it might have been.

“We’re expecting more action on antitrust enforcement in general. I’m not saying particularly in private equity,” said Shira Stein, a reporter at Bloomberg Law covering the federal response to Covid-19. “I don’t think they’re there yet or making those kinds of granular level decisions. Right now, they’re really focused on getting Covid under control.”

The Bottom Line

The healthcare industry is booming with transformative opportunities that make the room for more and bigger private equity deals in the next few years. With technology and value-based at its core, investors should always on the outlook for digitized medical practices that serve the needs of current and future patients. Yet they should also be careful of their acquisitions as rising threats can certainly be headline issues for PE involvement with healthcare industry.